4/8/2020 - Trading Lab Morning Email

After reaching a low of 2174 on the morning of March 23rd the S&P 500 has managed to rally nearly 27% against a backdrop of rapidly mounting COVID-19 deaths around the world. Not to mention the fact that the vast majority of the global economy is shuttered.

How can the market rise against this putrid backdrop you ask?

The simple answer is that the S&P had dropped nearly 40% in the month that preceded the March 23rd low. This drop was the sharpest in history and likely priced in much of the terrible outcome we are witnessing now. I also don't think I could have found a single bullish market participant on the morning of March 23rd, so it's natural that we have seen a short covering rally while the Fed, Treasury, and other global central banks douse markets with their biggest liquidity fire hoses.

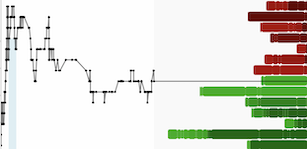

With that being said there is a very good chance that this counter-trend snapback rally reached its apex yesterday at 2757 on the S&P 500:

SPY (Daily)

Goldman Sachs analyst David Kostin (who correctly called for the market downturn last month) explains the asymmetry of the risk vs. reward in being long at S&P 2750:

“There’s a little bit of asymmetry in terms of the downside risk toward a level in the S&P 500 of around 2,000, which is down almost 25%, and upside of around 10% to a target at the end of the year of 3,000,” ~ David Kostin

Looking for 10% of potential upside while risking ~30% of downside doesn't sound like a good proposition to me. Judging by yesterday afternoon's sell-off some other market participants seem to agree.

I also couldn't help but notice that stock market sentiment has improved a lot in the last two weeks and people are looking for long setups again. The irony is that they should probably be doing the opposite.

While the worst case scenarios may now be off the table after it appears that governments are finally getting their acts together and people have awakened to the seriousness of the situation. We are now likely to enter a long slog of coping with the aftermath of COVID-19 and embracing a 'new normal' that won't be conducive to strong economic output (at least not like we are used to). Risk aversion in all forms is likely to become more prevalent across society and markets.

The world is also facing the potential for increased isolationism and protectionism between countries, and don't forget that the US is about to enter a very ugly election campaign cycle which will serve to inflame open wounds.

While I see some reason for hope and optimism a few months down the road, I prefer to curb my enthusiasm for the time being. Until further notice rallies are to be sold into, not bought.

DISCLAIMER: The work included in this article is based on current events, technical charts, company news releases, and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.